New Delhi: IDFC First Bank has reported a net profit of Rs 101.47 crore for July-September quarter of the current fiscal year, on account of healthy interest income.

For quarter ending September 30, the bank’s net interest income grew 22% to ₹1,660 crore as against ₹1,363 crore a year ago. IDFC Bank’s total income grew by 21% at Rs 2,288 crore in July-September period of 2020-21 from Rs 1,884 crore. Net interest income was up by 22 per cent at Rs 1,660 crore.

Despite COVID-19 pandemic impact, the quarter-on-quarter NII grew by 2%, the private sector lender added.

“The profit after tax for the half-year ended September 30, 2020, is reported at Rs 195 crore. Thus the bank reported three consecutive quarters of profitability,” IDFC First Bank said in a release.

“However, there was a 19 per cent fall in the bank’s income from fee and other sources at Rs 359 crore due to lower loan originations and reduced banking activity on account of COVID-19 pandemic,” it said in a press release.

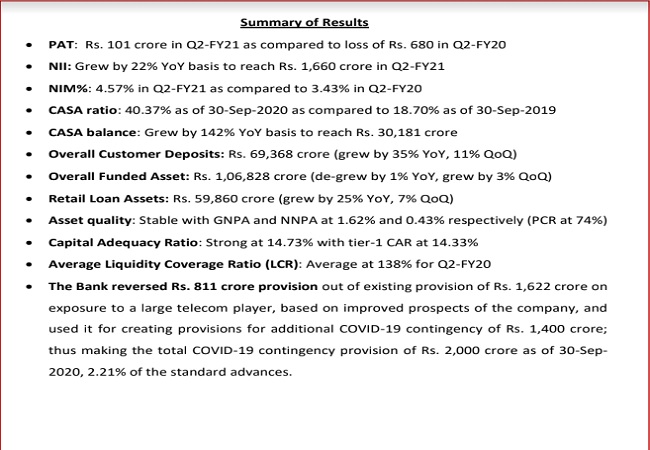

Financial results at a glance

Detailed note on Business & Financial Performance of Bank

Earnings

* Profit After Tax: The Profit after Tax for Q2 FY21 is reported at Rs. 101 crore as compared to Loss of Rs. 680 crore for Q2 FY20. The Profit after Tax for the half year ended September 30, 2020, is reported at Rs. 195 crore. Thus the Bank reported three consecutive quarters of profitability.

* Net Interest Income (NII): Net Interest Income (NII) grew by 22% Y-o-Y to Rs. 1,660 crore, up from Rs. 1,363 crore in Q2 FY20. Despite the COVID-19 pandemic impact, the Q-o-Q NII grew by 2%.

* Net Interest Margin (NIM%) (quarterly annualized): NIM% rose to 4.57% in Q2 FY21 from 3.43% in Q1 FY20 and 4.53% in Q1 FY21.

* Fee and Other Income (without trading gains): It decreased 19% to Rs. 291 Crore in Q2 FY21 as compared to Rs. 359 crore in Q2-FY20 due to lower loan originations and reduced banking activity on account of COVID-19 pandemic. However, sequentially, the Fee Income has shown significant improvement, up by 97%, as the economic activities are coming back on track post the phased unlock throughout the country. The trading gain for Q2-FY21 was at Rs. 337 crore.

* Total Income (net of Interest Expense): It grew by 21% at Rs. 2,288 crore for Q2-FY21 as compared to Rs. 1,884 crore for Q2-FY20.

* Release of Provisions on account of large telecom account: As of 30 June 2020, the Bank carried Rs. 1,622 crore of provisions, which were done proactively in Q3-FY20, against a large telecom exposure of Rs. 3,244 crore (Rs. 2,000 crore funded exposure through NCDs maturing in Dec-2021 / Jan-2022 and Rs. 1,244 crore of non-funded exposure through Bank Guarantee) as there were adverse comments around the future of the Company.

After the verdict of the Honourable Supreme Court on September 1, 2020, our assessment is:

1. The payment of AGR dues have been staggered which helps the Company with immediate cashflow. The DoT has allowed telecom operators to defer spectrum related payments due for two years (FY21-FY22) and pay it in instalments over next 10-14 years provided the operators arrange incremental BGs covering such payments.

2. Post AGR judgement, the Company has obtained approval from Board/ Shareholders to raise up to Rs. 25,000 crore through mix of debt (incl. convertible, hybrid instrument) and equity.

3. The Company has met all the borrowing obligations, including payment of Rs. 2,875 crore of NCDs in July 2020.

4. Subsequent to the SC decision on September 1, 2020, there have been trades in the NCDS issued by the Company maturing in January 2022 at a price of Rs. 80.5 to Rs. 81.7, i.e. a discount of ~19%.

Considering the positive outcome of AGR verdict and moratorium as described above, fund raising plan, repayment record and the recent trades, the Bank has released 50% provision out of Rs. 1,622 crore of provisions held as of June 30, 2020. The Bank continues to hold at Rs. 811 crore of provisions for the total exposure of Rs. 3,244 crore (25% PCR) on this telecom account as of September 30, 2020, as a prudent measure.

* Provisions: The provision for Q2-FY21 was at Rs. 676 crore as compared to Rs. 489 crore for Q2 FY20 and as compared to Rs. 764 crore in Q1 FY21.

Provisions for COVID-19 impact: As of 30 June 2020, the Bank carried Rs. 600 crore of provisions towards COVID-19 pandemic & related moratorium driven impact on its lending portfolio. As described above, Rs. 811 crore of provision was released from the existing provision done on a telecom player and has been utilized now to create additional provisions for COVID19 as a conservative measure. With this, during Q2-FY21, the Bank has taken additional provision of Rs. 1,400 crore towards COVID-19 to strengthen its balance sheet further. Including this, as of 30 September 2020, the Bank holds such provision of Rs. 2,000 crore which is 2.21% of its standard advances.

Liabilities – Strong and Steady growth

* CASA Deposits posted strong growth, rising 142% YoY to Rs. 30,181 crore as on September 30, 2020 as compared to Rs. 12,473 crore as on September 30, 2019.

* CASA Ratio improved to 40.37% as on September 30, 2020 as compared to 18.70% as on September 30, 2019 and 33.74% at June 30, 2020.

* Core Deposits (Retail CASA and Retail Term Deposits) increased 119% to Rs. 49,610 crore as on September 30, 2020 from Rs. 22,629 crore in September 30, 2019. This signifies the sticky and sustainable nature of the growing deposit balance.

* The Fixed Deposits of the Bank has the highest rating “FAAA/Stable” by CRISIL.

* Certificate of Deposits: The Bank has reduced its dependence on the wholesale and market borrowings which have been suitably replaced by the growth of core Retail Deposits. The borrowing through Certificate of Deposits (CD) of the Bank has reduced by 65% on YOY basis to Rs. 5,399 crore as on September 30, 2020 from Rs. 15,283 crore as of September 30, 2019.

* As of September 30, 2020, the Bank has 523 branches and 509 ATMs across the country.

Loans and Advances – stable with growing retail %

* Total Funded Loan Assets stood at Rs. 1,06,828 crore as on September 30, 2020, compared to Rs. 1,07,656 crore as on September 30, 2019, and as compared to Rs. 1,04,050 crore as on June 30, 2020. As per the stated strategy, the Bank focused on growing the retail loan book and decreased the wholesale loan book, primarily the infrastructure loans to reduce concentration risk on the portfolio.

* Retail Loan Book, out of the total book mentioned above, increased by 25% to Rs. 59,860 crore as on September 30, 2020, compared to Rs. 48,069 crore as on September 30, 2019.

* The Bank also has inorganic portfolio buyouts, primarily to cater to the PSL requirements where the underlying assets are retail loans. Retail loans including such inorganic portfolio constitute 63% of the overall loan assets.

* Wholesale Loan Book, including Security receipts and Loans converted to equity reduced by 20% from Rs. 49,269 crore as of September 30, 2019, and from Rs. 40,275 crore at June 30, 2020, to Rs. 39,286 crore as of September 30, 2020 as per the stated objective.

* Within the wholesale segment as stated above, the Infrastructure loan book reduced by 27% to Rs. 12,502 crore as on September 30, 2020 from Rs. 17,211 crore as on September 30, 2019 and Rs. 13,416 crore at June 30, 2020.

Asset Quality

* The Gross NPA of the Bank reduced to 1.62% as of September 30, 2020, as compared to 1.99% as of June 30, 2020. The Net NPA was 0.43% as of September 30, 2020, as compared to 0.51% as of June 30, 2020. The Gross NPA and Net NPA of the Bank was at 2.62% and 1.17% respectively as of September 30, 2019.

* This is after the impact of the Supreme Court of India notification to stop fresh NPA classification post August 31, 2020, till further orders. Without this impact the GNPA as on September 30, 2020 would have been 1.87% and the NNPA as on September 30, 2020 would have been 0.60%.

* As of September 30, 2020, the Gross NPA % of the Retail Loan Book was at 0.41% as compared to 0.87% as of June 30, 2020 and Net NPA % of the Retail Loan Book of the Bank was at 0.17% as compared to 0.24% as of June 30, 2020. Without considering the impact of Honorable Supreme Court’s notification the GNPA and NNPA of Retail Loan Book would have been 0.79% and 0.41% respectively. The Gross NPA and Net NPA for the retail loans of the Bank was at 2.31% and 1.08% respectively as of September 30, 2019.

* The Provision coverage ratio on NPA accounts improved to 74% at September 30, 2020 as compared to 56% at September 30, 2019 and 75% at June 30, 2020.

* Apart from the NPA, the identified stressed asset pool of the Bank, reduced by Rs. 827 crore during the last one year. This stressed pool stood at Rs. 2,717 crore as of September

30, 2020 against which the Bank has done provisioning of Rs. 1,303 crore, 48% of the pool. The Bank completely exited from its exposure towards a large HFC during the quarter at its carrying value in books.

Operations & Product Launches during the last quarter

* During Q2-FY21, the nation-wide lockdown due to COVID-19 pandemic got relaxed gradually across the nation.

* The loan disbursal levels across the product categories have improved every month and at a gross level the retail disbursals have reached 74% of the disbursal levels for the same quarter last year with the urban consumption-based retail products touching around 90% of the disbursal levels for same quarter last year.

* The Bank introduced the touchless debit card facility for its liability customers during the last quarter.

* During the quarter ended on September 30, 2020, the RBI announced the restructuring plan for the eligible customers with loan ticket sizes below Rs. 2 crore. The Bank has formed suitable policies to provide restructuring plans to eligible customers. The eligible customers can apply for such plan till December 31, 2020. As of September 30, 2020, the Bank has not received any sizeable request for restructuring.

Capital and Liquidity Position

* Capital Adequacy of the Bank was strong at 14.73% with CET-1 Ratio at 14.33% as of September 30, 2020, as compared to Capital Adequacy Ratio of 15.03% and CET-1 Ratio of 14.58% as of June 30, 2020.

* Average LCR for the quarter was at 138% which is much higher than the mandated regulatory levels.

Mr. V Vaidyanathan, Managing Director and CEO, IDFC FIRST Bank, said, “Since day one of the merger, our first priority was to strengthen the deposit side of the bank with stable retail deposits. We were very clear that we don’t want to grow the loan book until this is addressed. I am happy to say that IDFC FIRST Bank CASA ratio has reached industry best standards of over 40%. With the liability side firmly addressed, you will see growth in the total loan book from Q3 FY21 and onwards. I am further happy to inform you that the collection performance on retail loans have improved sharply after the lockdown has been lifted, and in fact are much stronger than earlier anticipated.”

About IDFC FIRST Bank

IDFC FIRST Bank was founded by the merger of IDFC Bank and Capital First in December 2018. The Bank provides a range of financial solutions to individuals, small businesses and corporates. The Bank offers savings and current accounts, NRI accounts, salary accounts, demat accounts, fixed and recurring deposits, home and personal loans, two-wheeler loans, consumer durable loans, small business loans, forex products, payment solutions and wealth management services. IDFC FIRST Bank has a nationwide presence and operates in the Retail Banking, Wholesale Banking and other Banking segments. Customers can choose where and how they want to Bank: 523 Bank liability branches, 128 asset branches, 509 ATMs and 654 rural business correspondent centres across the country, net Banking, mobile Banking and 24/7 toll free Banker-on-Call service.