New Delhi: The Board of Directors of Indiabulls Housing Finance Ltd. (IBH) announced its unaudited financial results for the quarter ended December 31st 2020.

The numbers are reported under Indian Accounting Standards [IndAS].

• As cost of funds moderate spread on loan book has expanded leading to rise in NII

• Strong traction in developer loan refinance pushing reduction in wholesale book

• Retail loan disbursals have picked up on the back of rising house sales

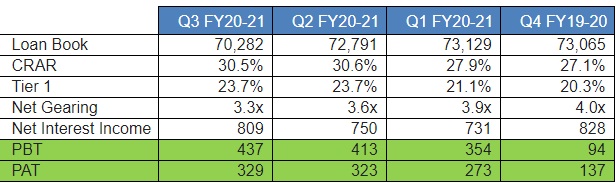

• PAT for 9MFY21 is ₹ 925 Cr and for Q3FY21 is ₹ 329 Cr – a growth of 2.0% QoQ

• On balance sheet loan book stands at ₹ 70,282 Cr on account of developer book run off through

refinancing. Retail loan book has grown

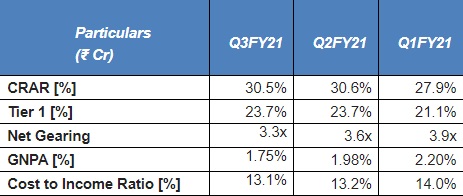

• Gross NPAs have remained moderate at 1.75%. Without the Supreme Court’s dispensation, Proforma Gross NPAs would be 2.44% compared with 2.21% at the end of Sep 30, 2020. Proforma [without Supreme Court dispensation] Gross NPA provision coverage ratio stands at 40%

• Capital adequacy stands at 30.5% and Tier 1 at 23.7%

• Access to funding has normalised. Since April 2020, IBH has raised total funding of ₹ 28,119 Cr

• Company’s liquidity buffer, including undrawn available sanctions, stood at ₹ 17,105 Cr as at end of Q3FY21, representing 24% of its on balance sheet loan book

• The Company’s ALM is fully matched for all granular buckets for 10 years and beyond. The company has a positive balance across all buckets, and will have a positive net cash of ₹ 13,965 Cr one year hence at the end of December 2021

• Mr. Dinabandhu Mohapatra, ex-MD & CEO of Bank of India, with over 35 years of banking experience has

been inducted into the Board

Funding flow has normalized:

Access to funding has normalised. The Company’s funding costs have moderated with cost of funds on book now down to 8.5%. This has helped expand the Company’s spread on book to 2.6%. In addition to availing funds at decreasing costs, the Company is also raising large sums of long term monies, of over 5 years tenure, which bodes well for its ALM. Overall, in FY21, the Company has raised a total of ₹ 28,119 Cr through equity, bank lines, bonds and loan sell downs.

Asset Quality:

The Company’s reported Gross NPAs as at end of December 2020 are at 1.75%. Without the Supreme Court directed standstill on asset classification, the proforma Gross NPAs would be 2.44% as at end of December 2020, compared with 2.21% at the end of Sep 2020. Had the Company not chosen to de-grow its book in the past 1 year, the proforma Gross NPAs of 2.44% would have been at 2.06%.

On Stage 3 assets, the Company has a provision coverage ratio of 40%. IBH has total provisions of ₹ 2,418 Cr on balance sheet which is equivalent to 3.4% of its loan book. Including accelerated write-offs effected by the Company [as IndAS does not permit creation of adhoc provisions] total provisions to loan book would be 5.0%.

Business Growth:

After going through a period of consolidation the Company has turned the corner and is now back on the path of growth. Net retail asset growth which started last quarter continued its momentum.

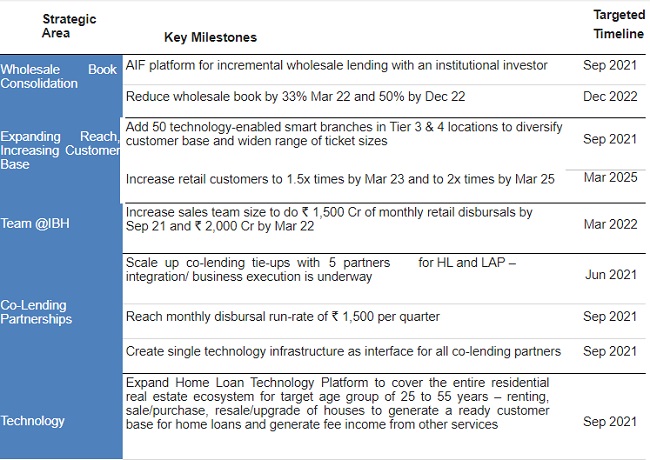

IBH’s disbursals have rebounded, with total disbursals in Q3FY21 of ₹ 3,458 Cr of which retail loan disbursals constituted 75% of the total. The Company is also seeing good traction in loan co-lending. The Company expects active sourcing to begin next quarter with 3 other co-lending tie-ups which are into the final stages of integration. Consequently, we expect the monthly disbursal run rate through co-lending to reach ₹ 1,500 Cr by September 2021.

We continue to de-risk our developer loan book through refinance and securitization of loans. We continue to see strong traction in developer loan refinance and are in talks with multiple financial institutions for sell down of this book. We expect to reduce our wholesale book by 33% by March 2022 and by 50% by December 2022.

On developer loans sourcing, we are in talks with 2 large real estate focused funds to set-up an investment platform. The talks have progressed well, and we expect to set up an investment platform by September 2021.

Appointment of Mr. Dinabandhu Mohapatra, ex-MD & CEO of Bank of India on the Board

Mr. Dinabandhu Mohapatra, ex-MD & CEO of Bank of India, with over 35 years of banking experience has been inducted into the Board.

Mr. Mohapatra has multi-dimensional banking experience across banking verticals, and will thus help guide in all facets of the Company’s operations to successfully achieve its targeted growth.

Affordability levels are at their best in over 2 decades on the back of low property price inflation and high wage inflation. This is further boosted by the prevalent benign interest rates. Supportive government policies like stamp duty cut by the state of Maharashtra, reduction in circle rates by 20% by the state of Delhi, announcement by the honourable finance minister to extend the tax benefits, by 1 year, for construction of affordable housing to builders and purchase of affordable segment houses by consumers and many more will make sure that the residential real estate industry is firing on all 3 cylinders of demand, supply and financing.

As per a Knight Frank report, housing sales volume in Q4CY2020 has already reached 100% of pre-COVID 2019 quarterly average. As per an estimation by Jefferies, residential sales in 2021 are expected to exceed 2019 levels by 10%, nearly doubling year-on-year, as the property cycle picks up. Unsold inventory too is on a decline having fallen by 9% YoY in Q4CY2020 and is expected to fall to 8 year lows by the end of 2021. Q4CY2020 also saw increase in residential project launches by 77% Q-o-Q which launches in premium segment accounting for 9% of the total launches. With the ongoing momentum in real estate, Jefferies expects launches to nearly double in 2021 year-on-year.