New Delhi: Amid some of the big companies facing an unstable stock market performance, the State Bank of India (SBI) has become the next giant for investors to eye on. After the Indian public sector bank announced March 2023 quarter-end results, its shares are anticipated to remain in the limelight.

Recently, SBI announced its increased March end net profits number of Rs 16,694.51 crore. The bank witnessed an 83.18 percent increase against Rs 9,113.53 crore in the previous March quarter. On the other hand, SBI’s net interest income for the March end quarter stood at Rs 40,392.50 crore, recording a 29.5 percent increase from last year’s same quarter figure of Rs 31,197 crore.

India’s largest lending bank further announced a dividend of Rs 11.30 per equity share in FY2023 which will be paid on June 14.

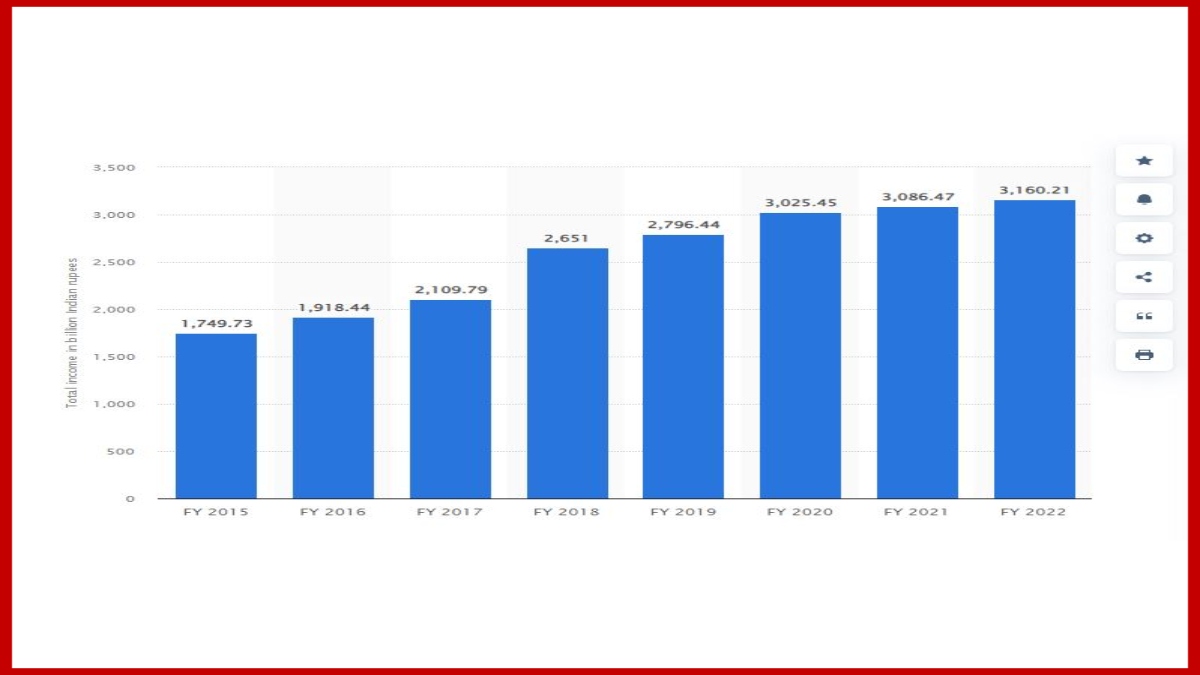

Indeed, the State Bank of India is on a spree of achieving milestones. According to Statista, the bank has marked a continuous surge in its total income from Rs 2,796.44 billion in FY 2019 to Rs 3,160.21 billion in FY 2022, resulting in the bank registering a brand value of US$ 7.5 billion in 2022.

Various brokerages have expected a healthy and balanced market performance of the bank. Motilal Oswal anticipated SBI FY25 RoA/RoE at 1.0%/ 17.1%. It has called for maintaining a buy but at an unchanged target price of Rs 700.

Meanwhile, Nirmal Bang analysed a healthy and balanced momentum considering SBI’s Q4FY23 results. It also analysed an improvement in SBI’s asset quality with higher recoveries and lower slippages. Nirmal Bang reiterated a buy with Rs 664 target price. Moreover, Morgan Stanley assigned a target price of Rs 715 per share, while analyzing the profit after tax (PAT) to be higher than anticipated.

All in all, the State Bank of India is on a spree of filling its bucket of success while expecting an upturn in its share prices as well.